IFRS S1 and S2 are the new global sustainability disclosure standards introduced by the International Sustainability Standards Board (ISSB). They aim to simplify sustainability reporting by creating consistent guidance for how companies disclose their climate and sustainability-related risks and opportunities.

With jurisdictions representing over 50% of global GDP already moving toward adoption, these standards are quickly becoming the new global baseline.

In this article, you’ll learn:

- What IFRS S1 and S2 are and how they work together

- Whether IFRS S1 and S2 are mandatory in your country

- What the key differences are between IFRS S1 and S2

- How ISSB compares to CSRD and TCFD

- Who needs to comply and when

- How platforms like Disclose help streamline IFRS S2 and ESRS E1 reporting

Whether you're navigating new disclosure laws like SB 261, preparing for the UK’s upcoming standards, or advising clients on global best practices, understanding IFRS S1 and S2 is essential.

What is the ISSB?

The International Sustainability Standards Board (ISSB) was established by the IFRS Foundation in 2021 to create a unified, global framework for sustainability-related financial disclosures.

Its goal is to eliminate the confusion caused by overlapping ESG standards by offering a single, investor-focused baseline.

Unlike earlier initiatives that were voluntary or region-specific, the ISSB’s standards are designed to be adopted by regulators, used by capital markets, and integrated into mainstream corporate reporting.

What does the ISSB do?

The ISSB develops disclosure standards that help companies explain how sustainability and climate-related risks affect their business performance, financial planning, and access to capital.

These standards are intended to:

- Align with existing frameworks like TCFD, SASB, and CDSB

- Enable companies to disclose comparable, decision-useful data

- Reduce duplication and inconsistency in sustainability reports

For example: A real estate investment firm with assets across the UK and California can use ISSB standards to report physical climate risk exposure in a format that satisfies both regional regulators and global investors without producing multiple reports tailored to each stakeholder.

What are IFRS S1 and IFRS S2?

IFRS S1 and IFRS S2 are the first two sustainability disclosure standards developed by the ISSB. They were released in June 2023 and came into effect for annual reporting periods starting on or after 1 January 2024.

The two standards are designed to work together:

- IFRS S1 sets the general standard for disclosing sustainability-related risks and opportunities.

- IFRS S2 focuses specifically on climate-related risks, including both physical and transition risks.

Both standards are aligned with the structure of the TCFD recommendations: Governance, Strategy, Risk Management, and Metrics & Targets.

What is IFRS S1?

IFRS S1 outlines how companies should disclose any sustainability-related risk or opportunity that could affect their financial position, performance, or access to capital.

It’s a broad sustainability standard that applies to environmental, social, and governance (ESG) topics, not just climate.

It includes:

- How sustainability factors affect business strategy and cash flow

- Materiality-based disclosure (i.e. what's relevant to investors)

- A requirement to report in the same timeframe and currency as financial statements

For example: A global logistics company using IFRS S1 would disclose how water scarcity, labour risks, or supply chain ethics affect long-term planning and investor outlook.

What is IFRS S2?

IFRS S2 focuses only on climate-related risks and opportunities. It requires companies to disclose:

- Exposure to physical climate risks (like flooding or heat stress)

- Exposure to transition risks (like decarbonisation policies or carbon pricing)

- Climate-related opportunities (such as clean energy investments)

- Scenario analysis and climate resilience planning

It also introduces new expectations, such as:

- Industry-specific metrics

- Disclosures on the use of carbon credits

- Reporting on financed emissions (for financial institutions)

For example: A renewable energy developer using IFRS S2 would need to report how their portfolio performs under a 1.5°C or 4°C scenario, and what transition risks affect future returns.

IFRS S1 vs IFRS S2: What’s the difference?

Although both standards are designed to improve transparency around sustainability-related risks, IFRS S1 and IFRS S2 serve different purposes.

- IFRS S1 provides the overall structure for sustainability disclosure across environmental, social, and governance (ESG) topics.

- IFRS S2 focuses specifically on climate-related financial risks and opportunities.

If you're reporting on climate risk, you'll use both standards: S1 sets the rules for how to disclose; S2 defines what to disclose on climate.

Comparison table: IFRS S1 vs IFRS S2

How the two standards work together

- Think of IFRS S1 as the architecture. It defines the structure, scope, and reporting principles for sustainability disclosures, including timing, materiality, and alignment with financial statements.

- IFRS S2 builds on that foundation with a specific focus on climate-related disclosures. It sets out what companies need to report about physical climate risks and opportunities, including governance, strategy, risk management, and metrics and targets.

For instance, a company reporting under IFRS S2 must also meet the general disclosure requirements of IFRS S1. That means applying the same reporting period, explaining materiality judgements, and ensuring consistency with financial reporting.

Are IFRS S1 and S2 mandatory?

IFRS S1 and S2 came into effect on 1 January 2024, but they are not automatically mandatory everywhere. Adoption depends on whether a country or regulator chooses to endorse them.

That said, momentum is building quickly.

As of mid-2025, over 20 jurisdictions, representing more than 50% of global GDP, have either adopted or are in the process of adopting the ISSB standards.

Which geographies have adopted or endorsed IFRS S1 and S2?

The following table highlights a selection of jurisdictions that have adopted, endorsed, or are in the process of aligning with IFRS S1 and S2.

This is a non-exhaustive list, as many countries are still developing their implementation plans.

When are IFRS S1 and S2 effective?

- The standards became effective from 1 January 2024 on a voluntary basis

- In some countries (e.g. Nigeria), they are already mandatory

- In others (e.g. UK, Canada), they will become mandatory from 2025 or 2026

- Many regulators are in consultation or preparing phased rollouts

Example: A UK-based asset manager will likely need to report using UK-endorsed ISSB standards from 2025 onwards. If they already follow TCFD, the transition will be relatively straightforward.

Who needs to comply with IFRS S1 and IFRS S2?

IFRS S1 and S2 apply to companies that operate in jurisdictions where these standards are adopted either as mandatory requirements or as the recommended reporting baseline.

In most cases, they target organisations that raise capital in public markets, manage large or cross-border portfolios, or have significant exposure to sustainability or climate risk.

But even where not mandatory, investors, insurers, and clients increasingly expect disclosures aligned with IFRS S1 and S2.

For example: A consultancy supporting a real estate fund with €2B in assets will likely need to help that client assess and disclose physical climate risks under IFRS S2 or CSRD, even if their home jurisdiction hasn’t made ISSB mandatory yet.

ISSB vs CSRD: What consultancies need to know

If you work with clients across both EU and non-EU markets, understanding how ISSB and CSRD compare is critical. Both frameworks aim to bring rigour and transparency to sustainability reporting, but they differ in scope, focus, and structure.

Key differences at a glance:

Why this matters for consultancies: If you support global or EU-based clients, you’ll often need to structure reports to cover both. That means mapping data points, aligning metrics, and avoiding duplication, which can be time-consuming without the right tools.

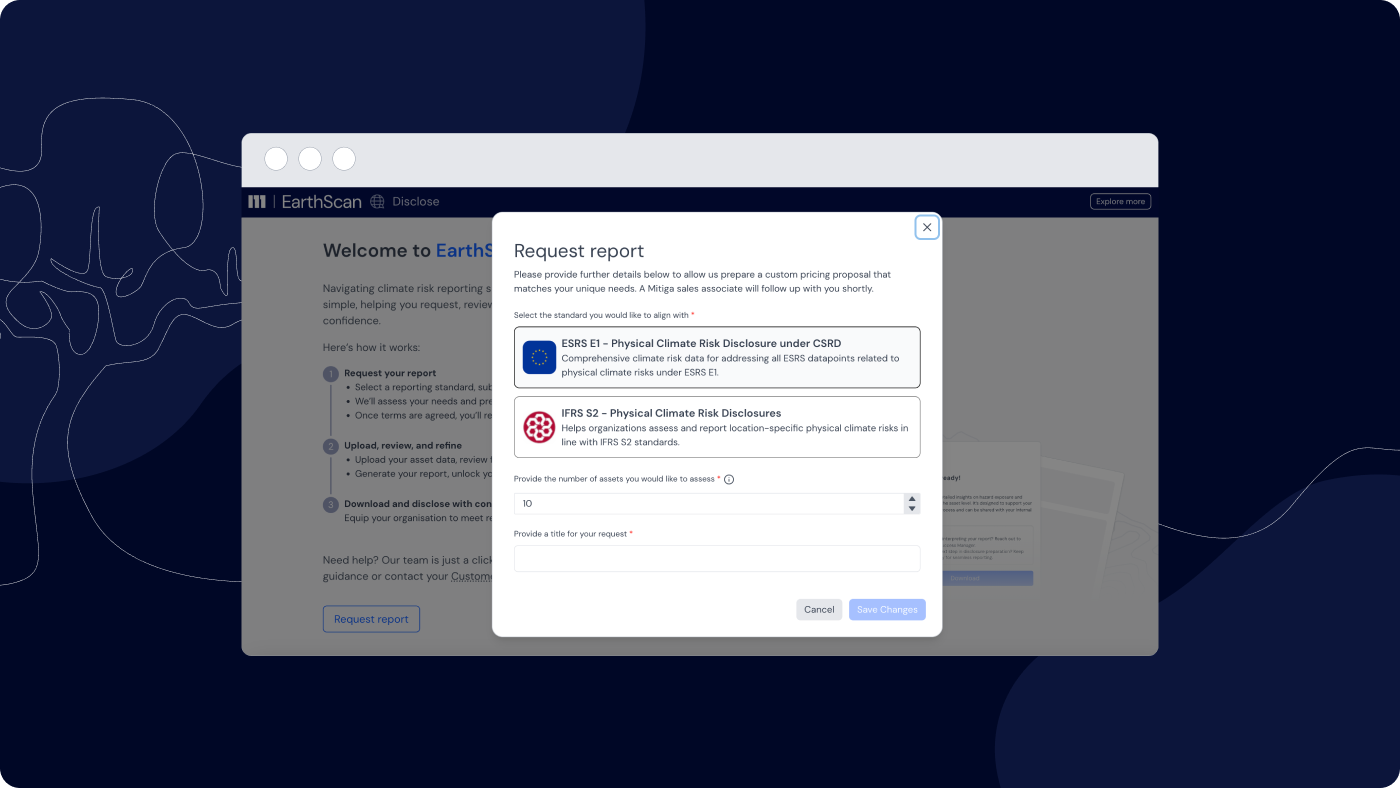

Reporting under IFRS S2? Disclose has you covered

Disclose is purpose-built to support organisations reporting under the world’s two most widely adopted climate risk disclosure standards:

- IFRS S2, issued by the ISSB

- ESRS E1, required under the EU’s CSRD regulation

With a single upload of your asset data, you can generate science-backed physical climate risk reports aligned with both standards, complete with hazard-level insights, scenario analysis, and financial metrics like Climate Value at Risk (CVaR).

Reports are automatically mapped to the disclosure fields required by each standard, removing the need for manual data wrangling or interpretation.

Aligned with global regulations like SB 261, UK SRS, and AASB 2

Because IFRS S2 is a recognised successor to TCFD, you can also use Disclose to align with regulations such as California’s SB 261, which requires companies to report on climate-related financial risks in line with TCFD or a successor framework.

The same applies to emerging standards like the UK Sustainability Disclosure Standards (UK SRS) and Australia’s Sustainability Reporting Standard S2: Climate-related Financial Disclosures (AASB S2), both of which are being built on IFRS S2.

That means a single Disclose report can support compliance across multiple jurisdictions, reducing duplication and helping teams respond to investor, board, and regulatory expectations with confidence.

Because IFRS S2 is now shaping climate risk disclosure rules around the world, Disclose supports alignment with key regulatory standards, including:

- SB 261 (California, US): Requires climate-related financial risk disclosures based on TCFD or a successor

- UK Sustainability Disclosure Standards (UK SRS): Upcoming standards based on IFRS S2

- AASB 2 (Australia): Australia's climate disclosure standard, closely aligned with IFRS S2

- CSRD (EU): Requires reporting under the European Sustainability Reporting Standards (ESRS), including ESRS E1 for climate

What you get with Disclose

- Per-asset climate risk data for 10 physical hazards: including flood, wildfire, drought, and heat stress, modelled using IPCC-aligned scenarios and Mitiga’s proprietary EarthScan engine

- Financial impact estimates: Climate Value at Risk (CVaR) is currently available for flood and extreme wind, calculated at the 50th percentile. Results are provided across short, medium, and long-term time horizons to help assess potential exposure over time.

- Disclosure-ready Excel reports: Outputs are fully mapped to IFRS S2 and ESRS E1 datapoints, structured for direct integration into regulatory filings

- Pre-drafted narratives: Automatically generated text aligned with regulatory language, ready to be reviewed and inserted into sustainability reports

- Real-time, scalable reporting: Upload your asset list and generate complete, assurance-friendly reports in minutes, without needing internal modellers or third-party companies to model data

Disclose is already trusted by consultants and corporates reporting under CSRD (ESRS S1) and aligning with global standards like IFRS S2.

It supports regulatory requirements across multiple jurisdictions, including SB 261 in California and the upcoming UK Sustainability Disclosure Standards (UK SRS), all from a single dashboard.

Fast, science-backed, and regulator-ready, Disclose simplifies your physical climate risk disclosure.

Final thoughts: What this means for consultancies

IFRS S1 and IFRS S2 represent a shift toward unified, investor-grade sustainability reporting. While adoption timelines vary, the direction is clear: more companies, in more places, will need to disclose climate risk and sustainability information with increasing rigour.

For consultancies, this is both a challenge and an opportunity:

- You’ll need to guide clients through new reporting requirements, fast.

- You’ll need tools that make multi-standard disclosure manageable.

- You’ll need to ensure outputs are credible, compliant, and investor-ready.

Disclose is one way to stay ahead. It turns physical climate risk data into pre-formatted, regulator-aligned reports that are easy to generate, explain, and defend.

Explore Disclose and see how it can support your clients’ IFRS S2 and ESRS E1 (CSRD) compliance.

FAQs about IFRS S1 and IFRS S2

What are IFRS S1 and IFRS S2?

IFRS S1 sets the overall requirements for disclosing sustainability-related risks and opportunities that could impact a company’s financial position, performance, or cash flows. IFRS S2 builds on this by focusing specifically on physical climate-related risks and opportunities, including governance, strategy, risk management, and metrics and targets related to climate.

What is the difference between IFRS S1 and IFRS S2?

IFRS S1 covers all sustainability issues. IFRS S2 is specific to physical climate risks and opportunities.

Are IFRS S1 and IFRS S2 mandatory?

Not everywhere. Some jurisdictions (like the UK and California) are aligning with them. Others use them as voluntary guidance.

When are IFRS S1 and IFRS S2 effective?

Both came into effect in January 2024, initially on a voluntary basis.

Who needs to comply with IFRS S1 and IFRS S2?

Primarily, large, listed companies, financial institutions, and those seeking to raise capital, especially in jurisdictions adopting ISSB.

Are IFRS S1 and IFRS S2 mandatory in the UK?

Not yet mandatory, but UK-endorsed versions are expected in 2025.

Which geographies are adopting IFRS S1 and IFRS S2?

UK, Canada, Brazil, Nigeria, Singapore, California, Australia, and others have announced alignment or consultations.

Does IFRS S2 align with SB 261?

Yes. IFRS S2 is fully aligned with the disclosure requirements of California’s SB 261.

While SB 261 does not mention IFRS S2 by name, it requires companies to disclose climate-related financial risks in line with the TCFD framework or a recognised successor. Since the International Sustainability Standards Board (ISSB) has incorporated all of TCFD’s recommendations into IFRS S2, this new global standard qualifies as a successor framework under SB 261.

That means companies can use IFRS S2 as a structured and globally recognised way to meet their obligations under SB 261 without starting from scratch or creating a separate reporting process.

Disclose simplifies this even further. The platform generates science-backed physical climate risk reports aligned with IFRS S2, including:

- Asset-level risk data across multiple climate scenarios and time horizons

- Financial impact metrics like Climate Value at Risk (CVaR)

- Pre-filled IFRS S2-aligned templates in Excel

- Clear outputs that can be used across SB 261, UK SRS, AASB S2, and beyond